MPesa vs UPI

In this article, we will talk about the second idea that we discussed last week. Specifically, the UPI vs MPesa Case.

There is a profound cultural and emotional attachment to physical money.

We all recognise that Money, in its physical form, has held significant cultural and emotional value across various societies. This materiality of cash is deeply embedded in cultural practices and beliefs, and these beliefs cut across religious boundaries. For instance, the discourse around Goddess Lakshmi emphasizes money’s sacredness, and rituals such as Bhoni (the first sale of the day) and the custom of not touching money with feet highlight its reverence. Praying to money and the tradition of giving Shagun (auspicious money) at weddings further underscore the role of physical cash as something that’s more than just a tool for economic transactions. In other words, there is a profound cultural and emotional attachment to physical money.

However, physical money comes with its fair share of problems.

In addition to being susceptible to theft and loss, there is a large cost associated with producing, distributing, and maintaining physical money. Governments and financial institutions invest substantial resources in minting coins and printing bills, as well as in ensuring their circulation and security. This includes measures to prevent counterfeiting, which has become increasingly sophisticated with advancements in technology. Additionally, the use of cash can facilitate illegal activities such as money laundering and tax evasion, as it allows transactions to be conducted anonymously. This lack of traceability makes it challenging for authorities to monitor and regulate illicit financial activities effectively.

This is where UPI and MPesa appear. They are both interesting ways of getting the digitization process kick started.

Digital money can help solve many of these problems. It also has the potential to enhance the money multiplier effect. The money multiplier effect refers to the process by which an initial deposit in a bank leads to a greater final increase in the total money supply due to the lending activities of banks. Digital money can significantly amplify this effect by (1) facilitating faster and more efficient transactions and (2) providing access to banking services for individuals who were previously unbanked or underbanked. These are definitely good things that can happen to the general public. Therefore, governments have taken a lot of effort in digitizing the economy. This is where UPI and MPesa appear. They are both interesting ways of getting the digitization process kick started. While they differ in terms of the technology and the implementation parts, they are philosophically united - and therefore, an interesting context in which we can study how changes in consumer behavior can be architected on a large scale.

A little bit of context

MPesa, launched in Kenya in 2007 by the telecom company Safaricom, is a mobile money service that allows users to store money on their mobile phones, send and receive money, and pay for goods and services. It’s like having a bank account on your phone, but it works even if you don’t have a smartphone or access to the internet. MPesa was designed to help people who didn’t have access to traditional banking services, making it incredibly popular in Kenya and other parts of Africa.

You can learn more about it here:

UPI, or Unified Payments Interface, is a digital payments system developed in India by the National Payments Corporation of India (NPCI). Launched in 2016, UPI allows users to link their bank accounts to a single mobile application and make instant, real-time payments 24/7. It’s like a super app for all your banking needs, enabling you to transfer money, pay bills, and shop online without needing to know the recipient’s bank account details—just their UPI ID or phone number.

You can learn more about it here:

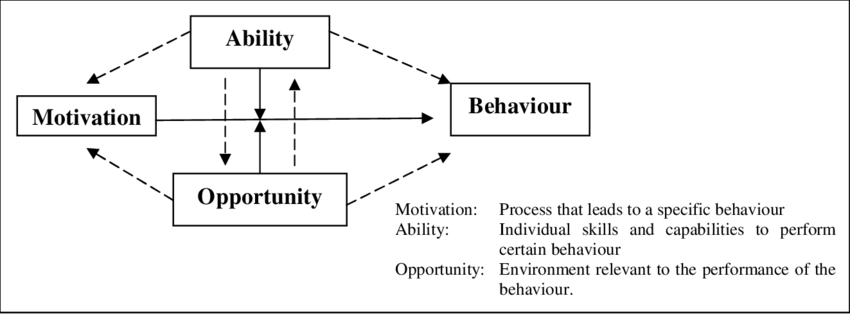

An introduction to the MOA framework

The MOA (Motivation, Ability, Opportunity) framework is a comprehensive model used to understand and influence consumer behavior by examining the factors that drive individuals to take action. The framework argues that Motivation, Ability, and Opportunity have a causal effect on Behaviour. (Scholars also have pointed out that the three variables are also interrelated, i.e. influence each other).

Let’s take a minute to discuss them in some detail.

Motivation refers to the internal drives and desires that prompt consumers to pursue certain behaviors, such as the need for convenience, security, or social status. Think of this as something similar to the electromotive force that allows electrons to move through circuits, except that it is inside our mind making us exhibit certain behaviors. In the case of UPI, you may be driven by the desire for better financial management and the convenience of tracking spending patterns in real-time.

Ability encompasses the skills and resources that consumers possess, enabling them to perform the desired behaviors, which may include financial means, technological proficiency, or access to information. For instance, a person with a smartphone and internet access, coupled with the know-how to navigate mobile banking apps, is able to exhibit cashless payment behavior.

Opportunity pertains to the external factors that facilitate or hinder consumer actions, such as the availability of digital payment systems, regulatory environments, or socio-cultural support. For example, the widespread deployment of mobile network infrastructure in rural areas provides residents the opportunity to access and utilize mobile banking services, while supportive government policies can encourage the adoption of digital payments by ensuring security and ease of use.

You see what we did there, did you not? We now have a framework that helps us think about the behavior that is being exhibited in a more systematic manner.

Businesses also use such frameworks to build their products and services. For instance, many firms use the MOA framework to effectively design strategies to enhance consumer engagement and drive adoption of innovations. This can be as basic as pouring the detergent into the washing machine more efficiently to ensure soap does not fall at other parts of the machine and damage it, to grander ideas such as promoting digital financial inclusion on a large scale.

Application of the framework

The MOA framework provides a robust lens through which we can analyze and predict the outcomes of technological innovations in the financial sector. When applied to the cases of MPesa in Kenya and UPI in India, the framework offers insights into why one succeeded while the other faced challenges.

Motivation in both contexts was initially high. MPesa was driven by the need to provide financial services to the unbanked population, while UPI aimed to enhance financial management and convenience for users in India. However, the difference in outcomes can be better understood by examining Ability and Opportunity.

Ability, which includes the skills and resources consumers possess, played a crucial role. In Kenya, the lack of widespread smartphone penetration and internet access limited the ability of users to fully leverage MPesa’s potential, despite its design to work on basic mobile phones. In contrast, India’s rapidly growing smartphone user base and improving internet infrastructure provided a fertile ground for UPI’s adoption. The widespread familiarity with mobile apps and digital interfaces among Indian consumers further enhanced their ability to adopt UPI seamlessly.

The combination of these events created an unprecedented opportunity for UPI to thrive.

Opportunity, the external factors facilitating or hindering consumer actions, was perhaps the most decisive factor. The Indian government’s demonetization initiative in 2016, which rendered high-denomination currency notes invalid, created a significant push towards digital payments. This sudden move disrupted traditional cash-based transactions, making digital alternatives like UPI not just convenient but necessary. Additionally, the COVID-19 pandemic further accelerated this shift by highlighting the need for contactless transactions to ensure safety and hygiene. The combination of these events created an unprecedented opportunity for UPI to thrive, as consumers sought out digital payment solutions that were both secure and efficient.

MPesa, on the other hand, faced different opportunity-related challenges. While it did achieve success in Kenya, its expansion into other markets was hindered by varying regulatory environments, differing cultural attitudes towards mobile money, and competition from established financial institutions. These external barriers limited the widespread adoption of MPesa outside Kenya.

Part of the reason why MPesa did not succeed could have also been due to the undesirable behaviors (such as gambling, debt taking) that MPesa enabled. Therefore, as budding businesspeople, you should think not just about the behavior that you have in focus, but also the other behaviors the same set of actions can kick start. If these ‘side effects’ cause issues that are undesirable to certain stakeholders, chances are, they would dissuade consumers from picking up the behavior and exhibiting it.

Conclusion

In conclusion, the MOA framework provides a valuable tool for understanding and influencing consumer behavior. In this episode of consumer behaviour, we looked at one particular context thats of interest to all of us - financial innovations. The contrasting outcomes of MPesa and UPI underscore the importance of aligning motivation, ability, and opportunity to drive successful adoption. While MPesa successfully addressed a critical need in Kenya, its challenges in expanding beyond its home market highlight the necessity of considering broader regulatory, cultural, and competitive factors. Conversely, UPI’s triumph in India was bolstered by significant external events like demonetization and the COVID-19 pandemic, which created a unique opportunity for digital payment systems to flourish.

Surely, you can use the framework in other settings where behavioural changes are being architected too. Simply grasping these ideas will help you gain a deeper understanding of consumer behavior.